When we’re traveling within the U.S., I don’t give much thought to travel insurance before the trip. I make sure to use a credit card with good travel protections, and if I rent a car, I use a card that acts as the primary coverage if there’s damage to the vehicle. For medical coverage, I’ll have my insurance card in my wallet if I get sick or even worse if there’s some sort of emergency.

When traveling outside the United States, there are a bunch of things to think about. You need to reconfirm travel arrangements, make sure you have all the necessary travel documents and visas and arrange for your mail to be held, your pets to be looked after and everything else that goes through your head. It’s easy to forget that you should also consider buying a travel medical insurance policy for your trip.

That’s because even if your medical insurance reimburses you for expenses abroad, they will most likely be considered out-of-network charges with high deductibles and copays. If you have Medicare, you don’t have any coverage at all.

According to an article from Consumer Reports,

“Most domestic health plans provide limited coverage overseas and won’t cover prescriptions abroad,” says Margaret Wilson, M.D., chief medical officer of UnitedHealthcare Global, which is part of UnitedHealthcare, the largest health insurer in the U.S.

If your insurer does provide coverage for medical treatment you get in another country, the care is typically reimbursed at an out-of-network rate, which means higher out-of-pocket costs.

So while medical costs outside the U.S. may be lower than what we’re used to here, I don’t want to pay out of pocket if I need to see a doctor while I’m away.

How to find an insurance company

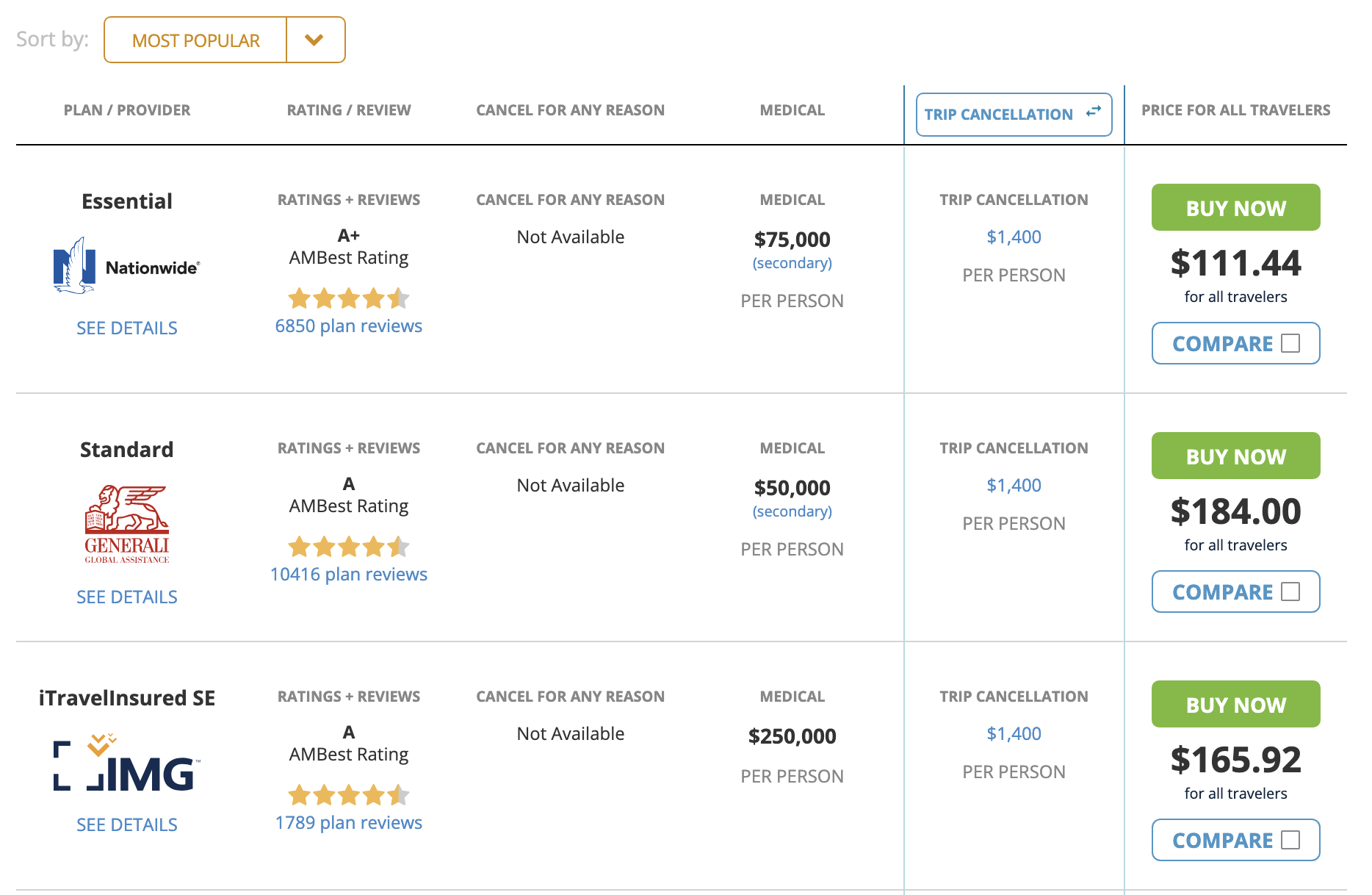

I don’t know about you, but I really don’t want to spend time searching around websites of insurance companies comparing policies. I’ve found that in this instance, using a comparison-shopping website works best for my needs. For as long as I can remember, I’ve used InsureMyTrip.com. I can’t say if they’re the best, easiest to use or the cheapest website but I’ve always been able to find coverages for our trips. All you need to do is plug in the information about your trip (countries visited, activities planned and dates of travel) and some personal information (the ages of the travelers is all they ask for a quote). The website searches for policies from many different insurance providers. They even provide information about what coverage policies provide if your plans change due to COVID-19 either before or during your trip.

The default setting is for a comprehensive policy which includes:

- Trip delay, cancellation, and interruption

- Baggage delay or loss

- Accidental death

- Medical Evacuation

- Medical and dental coverage

- and other coverages

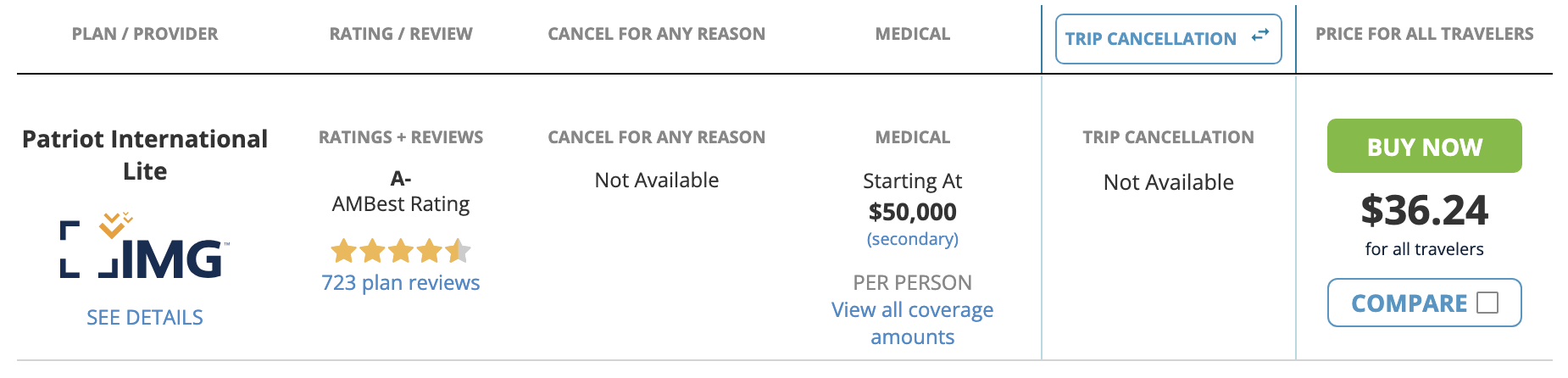

The site makes it easy to compare plans from different providers or even the various options from the same company. For our trip, many of the trip protections I already get from using our Sapphire Reserve card for the reservations, so I narrowed the search to medical policies.

The site makes it easy to compare plans from different providers or even the various options from the same company. For our trip, many of the trip protections I already get from using our Sapphire Reserve card for the reservations, so I narrowed the search to medical policies.

By eliminating travel protections, the prices go way down. Now, these prices are for the two of us for a 5-day trip. Compared to the cost of the trip, medical insurance is a negligible additional expense.

By eliminating travel protections, the prices go way down. Now, these prices are for the two of us for a 5-day trip. Compared to the cost of the trip, medical insurance is a negligible additional expense.

The premiums will vary based on your age, where you’re traveling, the level of coverage you choose and the duration of your trip. Several countries require you to have medical coverage to enter.

If you travel outside the U.S. several times a year, it may make sense to purchase a multi-trip policy.

Final Thoughts

I wouldn’t think of traveling outside the United States without having medical coverage. This doesn’t mean that I’ve forgotten until the day before the trip to purchase the policy. Fortunately, unlike getting other types of insurance, the process is quick and straightforward. I’m sure I might be able to find a better price if I went around and searched policies myself, but since the price is already relatively low, this is an instance where I’m happy to save some time even if I have to pay a few extra dollars.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

11 comments

People should consider their risk profile and healthcare costs in the country they’re visiting. Yeah, you often pay out-of-network costs for a visit abroad … but in some countries in Europe, your total liability for an ER visit might be $150. There is 1-2 orders of magnitude less personal cost exposure than in the US.

I’m just starting the research for Medicare and Medigap plans, etc. I therefore don’t know all the details, but I know some Medigaps show covering foreign travel medical costs.

Plain Medicare does not provide coverage but gap plans or Advantage programs might as an added incentive.

Super helpful stuff. Thanks. Like you, I use a credit card that has some decent protections and Blue Cross covers me internationally, but medevac can be insanely expensive.

Canada is cheap for Canadians but they charge more than it cost in the US if you are a foreigner (including an American) that shows up in a Canadian emergency room.

I check my health insurance to see if I’m covered (and I am) but I do risk not getting insured for evacuation back to the US.

For the past 4-5 years, I’ve changed my travel policy. I will no longer travel to a country that medical care is very poor. Even countries with good medical care have rural and isolated areas that have poor care. For example, there’s not a neurosurgeon skilled in head trauma in every US county. In Alaska, there are huge gaps, not covered. Some specialties are only barely covered in Anchorage.

I just got a quote for my wife and I for our next international trip and ran across a substantial problem: The medical insurance that is offered is all secondary coverage. In practical terms that means that if I’m laid up in a hospital in Bali, my regular health insurance provider and the additional coverage provider will be straining to have each other pay as much as possible of my bills. Meanwhile the hospital wants their money NOW while I’m sick and in the middle of the two parties who are not anxious to pay anytime soon and I will not be allowed to leave until my large medical expenses are paid. Secondary insurance coverage is fine for situations where there’s time to sort things out but awful for international emergencies where there’s potentially alternative coverage.

If I recall correctly, Amex Platinum provides evacuation assistance for cardholders and immediately family. I remember reading about a case where a cardholder sustained a head injury while mountain biking in Central America, and ended up in the hospital. Amex chartered a private jet along with a doctor, nurse and the cardholder’s spouse and paid to fly them stateside.

There is another website that acts as a travel insurance marketplace: Squaremouth.com. Also, do not assume that Chase Sapphire insurance will pay what you are not insuring because in my experience, CSR is some of the worst insurance offered. They will find a way to not cover your claim. For car rentals Chase Sapphire is fine, for other things it is terrible. As for covering only medical expenses, that is very short sighted. The most common injury for tourists is getting hit by a car as a pedestrian. Especially true in countries that drive on the left. If your injury is severe, you most definitely will need medical evacuation insurance as this can be your biggest expense. The policy you’re displaying does not cover medical evacuation. While Amex Platinum offers medical evacuation, their provider has to approve your situation. But you don’t have to charge your trip on the Amex card, it is just a benefit to cardholders.

Trip insurance should cover things that may cost you a large amount of money to pay yourself. I always recommend it for expensive trips that have multiple components that are unrefundable.

Another concern is for those that have pre-existing conditions. Most insurance carriers require that you purchase your policy with 2-3 weeks after purchasing (or reserving) your first travel component of the trip. That is if you wish to cover pre-existing conditions. This means if you reserve an award ticket that is considered your first purchase. If you do not purchase your policy in that time period, to cover pre-existing conditions, you have to purchase much more expensive policies to cover pre-existing conditions. Also, do not lie in the interview about these dates, because if you have to make a claim, the carrier will ask for original receipts on everything. So, if you fudge on the dates, your claim may be denied.

Trip insurance is not an item to be taken lightly. If you have health issues or doing an expensive trip, purchasing trip insurance should be foremost in your mind.

My Medicare part B supplement (Mutual of Omaha) to my standard Medicare policy covers $50,000 on international medical expenses . This is not a Medigap plan. My insurance broker tells me that this is a standard feature of all part B supplemental plans. This should be more than plenty if you are traveling in Europe, most of South America/ Caribean, Australia, Japan and similarly equipped countries.. But if you are more adventurous (e.g. an African Safari) then by all means include extra medivac coverage.

Thanks for the info; did my research and bought medical insurance for an upcoming Asian trip.

There is a large country in South Asia where you do NOT want to be injured in. Health care looks ok on the surface but is really terrible. There is a company that will evacuate you if you are in the hospital. I was thinking of getting that but didn’t. I think it was between $100 and $200 for a short trip but there is a yearly plan.