Note: Offers mentioned in this article are no longer available.

Over the course of one week, I dealt with issues from three different banks. Needless to say, that was one long week. I don’t understand why, when dealing with a bank, every transaction must be difficult. It’s like pulling teeth to get anything accomplished. When everything is difficult, I tend to get introspective and think, “Maybe I’m the one that’s difficult to deal with.” I’m looking for some objective opinions, is it me or is it the bank?

Situation 1

I signed up for the JetBlue credit card from Barclays, as I wanted to get the 60,000 points sign up bonus. After receiving the card I went online to activate it. That was easy and it showed up on my account online immediately. One of the pages during the activation process asked me to set up the card for mobile payments so when I was finished I went to add the card to Apple Pay on my iPhone.

The setup process for adding the card to Apple Pay was simple, as it tends to be for most other cards. However, at the end of the process, it said I needed to verify my identity and I needed to call the number provided. Whatever, I clicked on the number and was connected to Barclays.

Here’s where the call gets a bit strange. I had to give all of my identifying information to the first call rep, who eventually figured out why I was calling. She needed to connect me to the mobile payments department. So I sat on hold and was connected to a representative who explained that he’d have to confirm some details for them to activate Apple Pay on my iPhone with a Barclays card. Sure. Go ahead. What do you need to know?

- Which one of these licenses do you hold?

- What are the first 4 numbers on your drivers license?

- Which one of these is a previous address?

- At which one of these companies are you a former employer?

Apparently, I got one of these wrong, as I was then asked information about the amount of my mortgage payment, the most recent credit I’ve applied for and other financial and personal information.

I guess they were finally satisfied that I was who I claimed to be, as he then thanked me for being a Barclays customer and I could now use my JetBlue card on my phone. He did also say that these questions were only because I was a new customer (Hello, I’ve had two Aviator Red cards already and used them on Apple Pay) and in the future, I’d only be asked to confirm a code sent to me by email or text.

This took me about 10 minutes to complete but was way harder than I thought it should be. Is Barclays having so much trouble with fraud from mobile payments on new card applications? I was chuckling because it was them who asked me to enroll my card for mobile payments and had I known the hassle involved, I might not have bothered.

Situation 2

Our credit card number was hacked. Now, I don’t blame the bank for that, as it was totally out of their control. Even our call to report the fraudulent charge was handled OK. I mean, there were many things I think could have been dealt with better. I’ll explain…

I noticed a charge on our statement that we didn’t make. I immediately called the bank to inform them of the fraudulent charge and that we needed to get a new card number. The representative on the phone was competent in closing our account. When we mentioned that this card was set up for many online payments and we’d need the new number ASAP, she said they would overnight the card via FedEx to us, which was exactly what happened. We received the card within two days of reporting it being hacked.

Now here’s where the story gets weird. The card that was hacked was our Citi Prestige card. It’s a metal card and even the paperwork with the new card warned us against putting it into a shredder and we should contact Citi for disposal instructions.

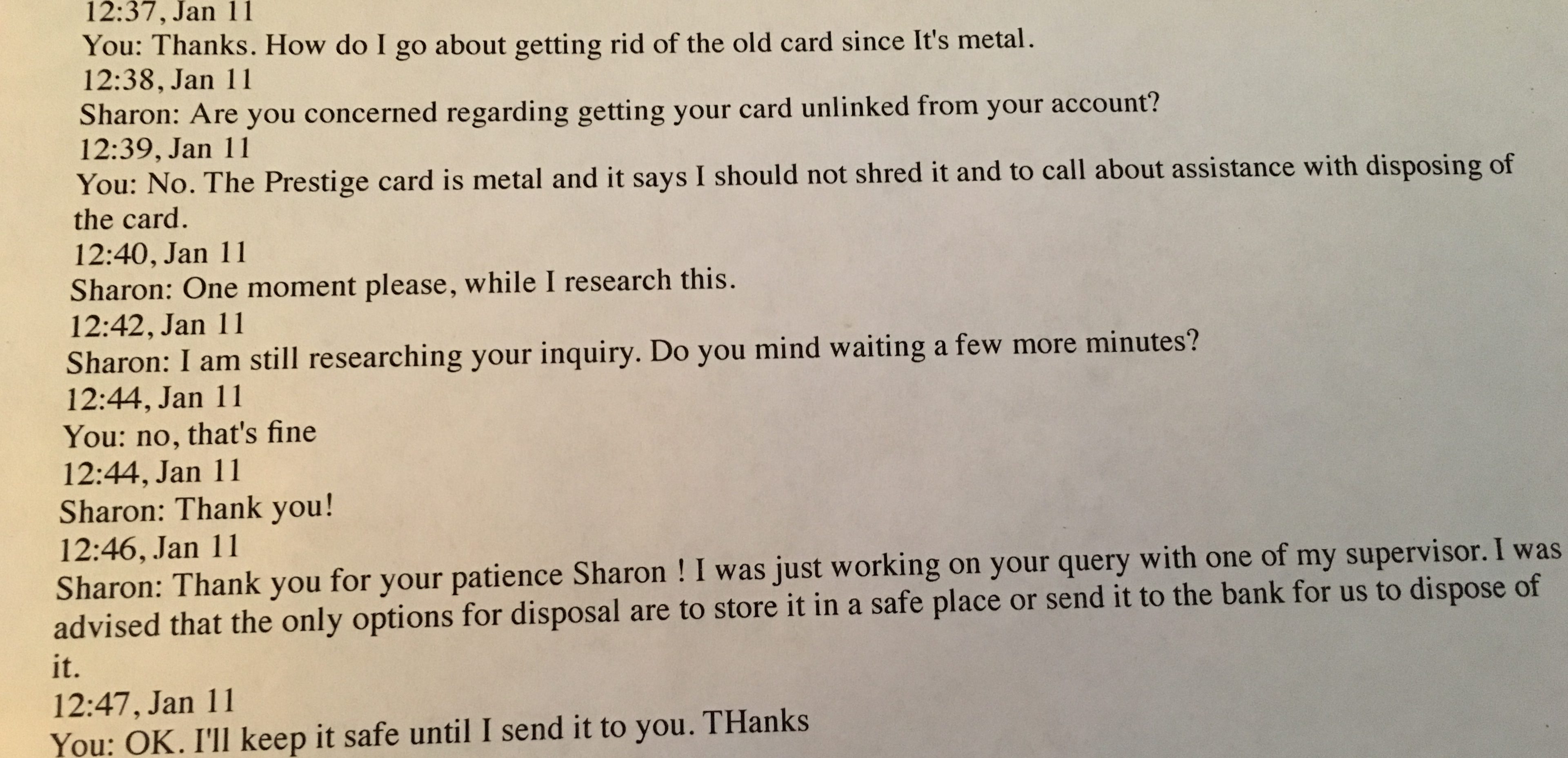

Sharon contacted them via online chat to find out how she should dispose of the card. Here’s how the chat went.

After a pause and speaking to a supervisor, the suggestion was to store the card in a safe place (for forever???)…or to send it back to the bank for disposal. It was clear the person she was chatting with had no idea the card was metal or how to dispose of it properly.

Sharon decided, smartly, to not ask how we should send it back to the bank via the chat session. Instead, she reached out to Citi on Twitter at @AskCiti. A quick response to a tweet on how to dispose of the card led to a DM saying they needed a phone call in order to send a mailer to dispose of the card. Sharon replied and within a few hours, we received a call from Citi’s social media team finalizing the details. At least one area of Citi has their act together.

Should this have been that difficult? Could there be a link on the Citi Prestige page for you to request a mailer online? Am I being difficult?

Situation 3

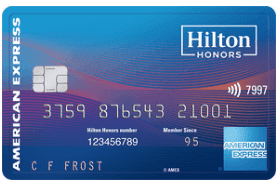

I had Sharon apply for the Citi Hilton Reserve card before it was closed to new applicants. After reaching the minimum spending we received the vouchers for the two free weekend nights, which we ended up using at the Casa Marina in Key West. The Citi Hilton card was being discontinued, so I had her call to cancel the card before it was transferred to the Hilton Ascend AMEX.

You could imagine my surprise when I saw this arrive in the mail:

American Express sent a new Ascend AMEX Hilton card on a canceled account. After chatting with several other people in the same situation, I was referred to a page on the AMEX site with this information:

Why did I receive a Hilton Honors American Express Card after cancelling my Citi Hilton Honors Card?

If you cancelled your Citi Hilton Honors Card between November 17, 2017 and January 30, 2018, you may still receive a Hilton Honors American Express Card in the mail. However, the Card will not be activated or available to use at the point of sale as your account will not be transferred to American Express. If you are unsure about the status of your account, you may call American Express starting on January 30, 2018 using the number on the back of the Card to confirm your account status.

So Sharon was sent a card that is not active and that she can’t use, but I have to wait two weeks before I can call the number on the back of the card to make sure she doesn’t have an account. Will this non-active account count against her getting this card for the sign-up bonus in the future (AMEX only allows one sign up bonus per LIFETIME) and will this non-active card show up on her credit report (important since Chase only allows five cards per 24 months)? No idea about the answers to these questions as any requests have to wait until 1/30/18.

It is just me? Why do banks do this? Should it be so hard? I’m getting a sense of why one of my friends on Facebook used to post FUBoA every other week because of her biweekly transactions with Bank of America. Please let me know it’s not me being irrational. It shouldn’t be this hard, should it?

Like this post? Please share it! We have plenty more just like it and would love if you decided to hang around and clicked the button on the top (if you’re on your computer) or the bottom (if you’re on your phone/tablet) of this page to follow our blog and get emailed notifications of when we post (it’s usually just two or three times a day). Or maybe you’d like to join our Facebook group, where we talk and ask questions about travel (including Disney parks), creative ways to earn frequent flyer miles and hotel points, how to save money on or for your trips, get access to travel articles you may not see otherwise, etc. Whether you’ve read our posts before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

1 comment

It’s the banks, not you. They treat us like inconvenience nuisances rather than valued customers. Need a statement that would take them 5 minutes to create and email? That’ll take 2 days. Oh, you want it mailed to you? That’ll take 9 days.